.svg)

.png)

Mortgage rates have gone from 2.5% to 7% in the course of a year.

That’s a 180% rally.

Where a $1,000,000 house could’ve been afforded on a $144,000 household income, now you’d need a $216,000 household income.

And that is assuming you have a good credit score, have no down payment, wanted to keep 50% of your income past your mortgage payment, and could magically get the prime rate on your mortgage.

Not to mention the fact that a $1,000,000 house a year ago could be worth ~$1,210,000 today. This means you would likely need a $252,000 salary today to buy the same house that you could on your $144,000 salary a year ago.

It’s no wonder the housing market is cooling off, but there are still buyers.

I believe there are fundamentally three things that are making mortgage rates balloon.

Demand

Supply and demand are everything in finance and economics.

When there is more money in excess, more money will be used to buy things. That’s the demand piece, that’s how we got high inflation, higher home prices, and lower mortgage rates.

People were competing for a relatively similar number of homes on the market with dollars given to them in excess. This meant the banks all had to compete vigorously on who gave the best rate to attract these buyers.

More dollars and borrowed dollars competing for the same number of homes meant mortgage rates and home prices became detached.

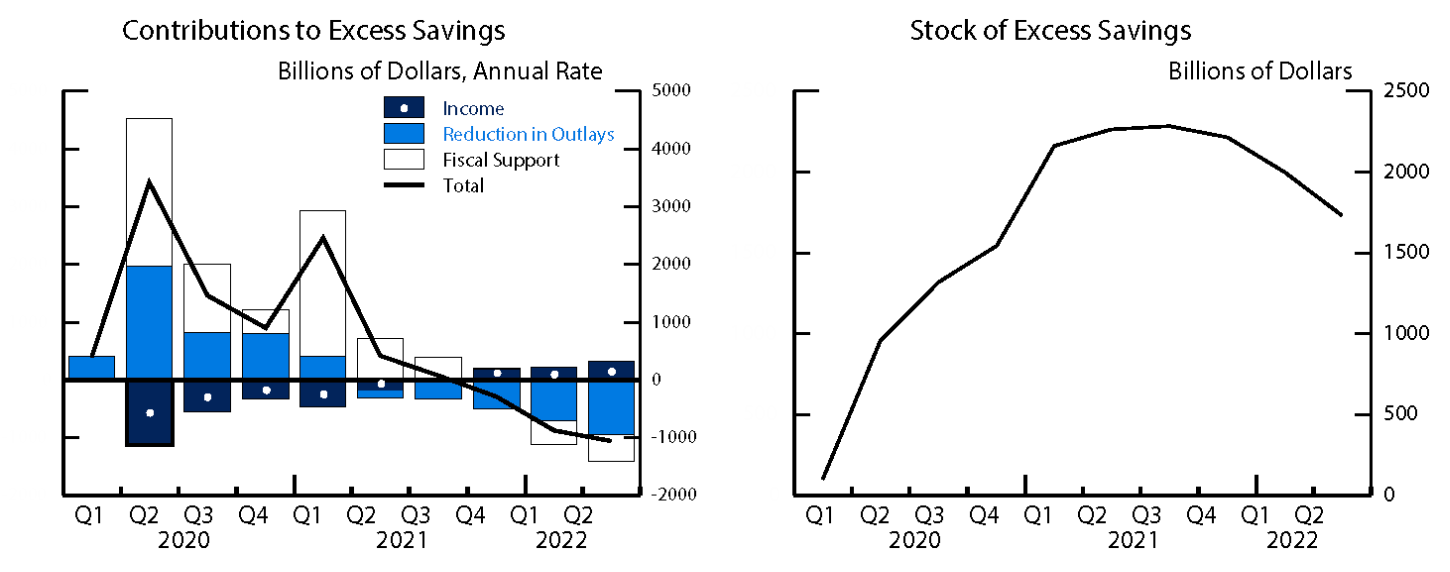

Here is where we are at with excess savings, people still have excess savings, and they will use them until there is nothing left. That is just consumer behavior.

Because there are still more excess dollars in the system people still have the buying power to go out and try to buy a house, meaning demand for mortgages and houses is still in the market.

Banks aren’t lending as much

Banks are required to keep a certain number of deposits in reserves so they don’t have issues like FTX and other crypto “banks” did.

Well because their economists have been warning about a pending recession they have been loading up on reserves.

That means that when you deposit your money in a bank maybe only $1 per every $10 went to reserves in 2020, now $5 out of $10 are going into reserves.

That means banks aren’t lending new money.

This is significant because this affects the supply of mortgages available to buyers, who still have an appetite for homes.

Less supply and similar demand means higher borrowing costs, ie higher mortgage rates.

The Function of Interest Rates

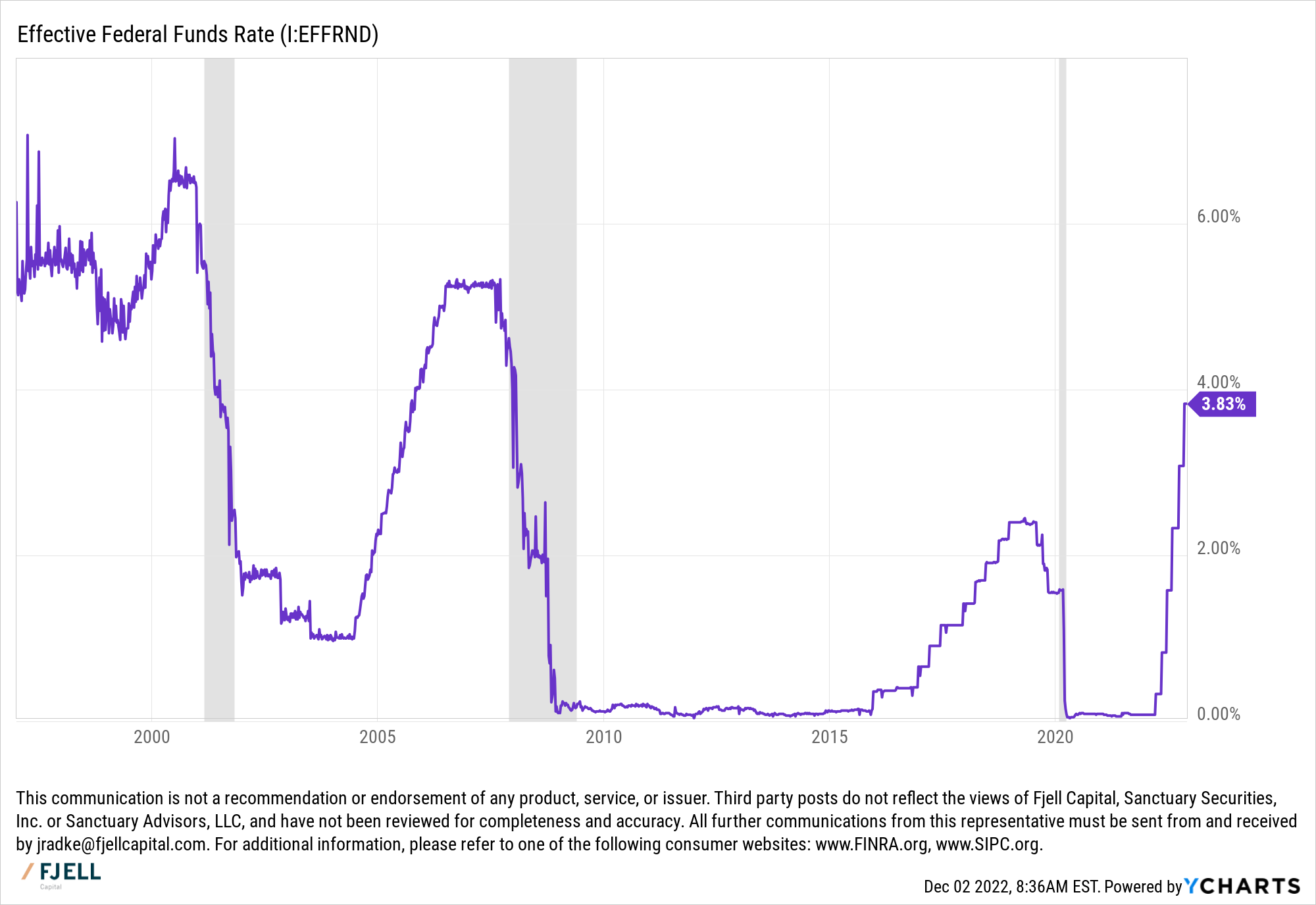

And of course, I can’t leave out the good ole Federal Reserve.

They have been raising the base interest rate since the beginning of 2022 meaning the output in the function of interest rates has changed.

Interest Rate = Base Rate + Credit Premium + Inflation Premium + Maturity Premium + …

When the base rate goes from 0% to 3% the final interest rate must rise by at least 3%, unless there are negative premiums associated with the function, which is unlikely to occur.

These Three Forces Put Together Makes The High Rate

Similar demand from savings + low supplied mortgages + higher base interest rates = higher mortgage rates.

The 30-year mortgage rate in the chart below is considered to be the rate issued to borrowers of the highest credit quality, and the US high yield BB effective yield is considered to be the highest rate junk bonds issued by US corporations.

Should the highest-rated individuals be considered as high risk as what are considered junk bonds? Probably not.

The idea is people might not buy a new mattress in a recession but they will for sure pay their mortgage, making mortgages a fairly safe place to invest during a recession (unless there are some really bad things going on).

So what this chart tells me is that mortgage rates will have to come down in the next 12-24 months for 3 reasons.

More supplied mortgages + lower demand + a steady or falling base rate = lower mortgage rates.

Plain and simple.

What I see is the potential for a prime mortgage rate of 4-5% in 2024, being that the Fed isn’t going back to near-zero interest rates in the foreseeable future.