.svg)

.png)

While there is no definitive name to what we experienced in 2021-2022, besides what some are calling “The Great Inflation”. I believe that we are mostly past that.

Now we are in what I will dub “The Great De-Inflation”. A period where inflation, and at some point interest rates, will revert back to their long run averages.

For inflation that’s 2% and for interest rates that should be somewhere between 2.5% and 3.5%.

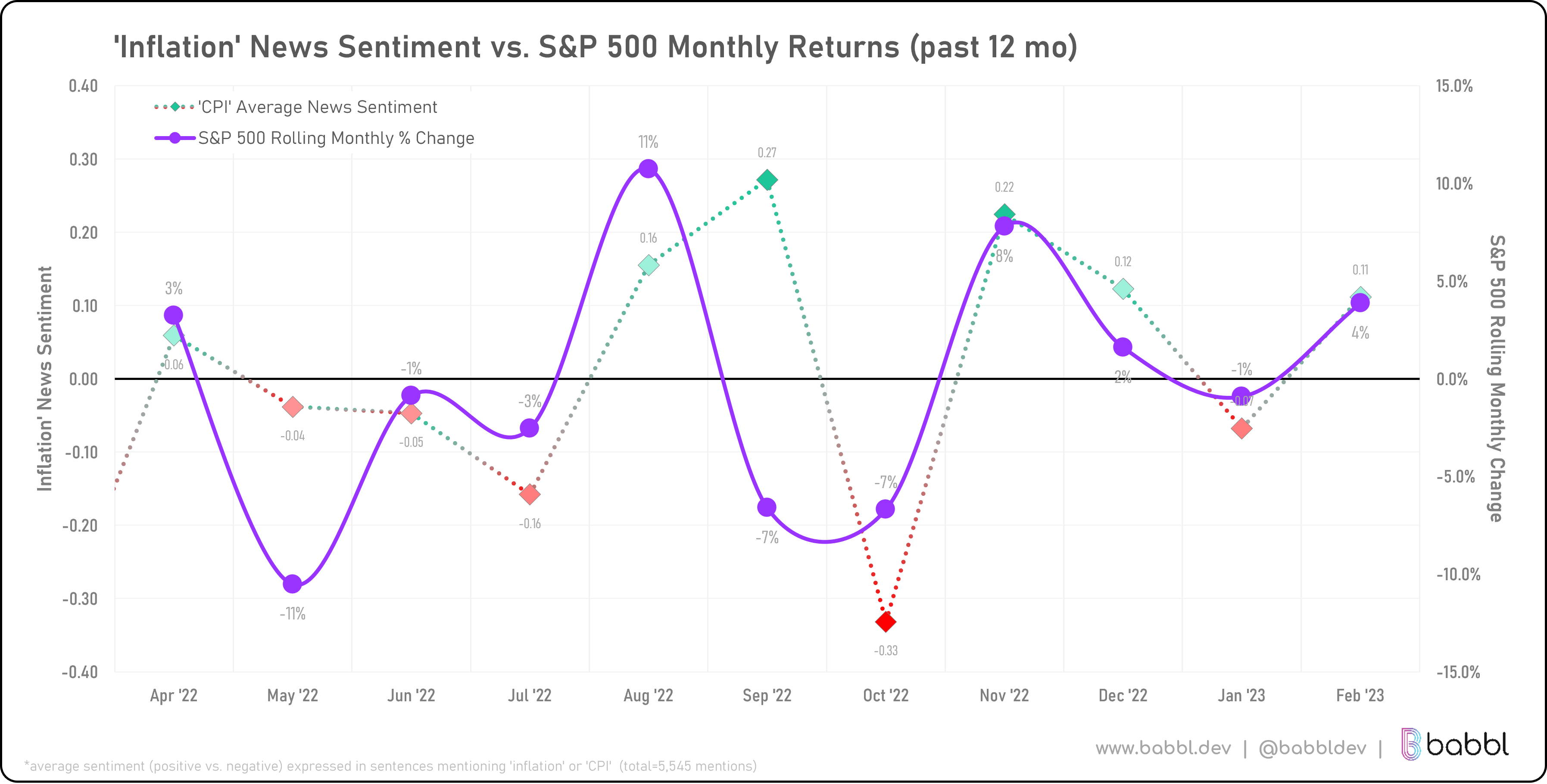

On Monday I had the opportunity to share some of my thoughts on inflation sentiment on Babbl’s Market Mood Newsletter.

The premise was that inflation was heavily weighted in the minds of investors in 2022. That meant small or large changes in inflation sentiment actually had a material effect on the stock and bond markets, as displayed in the chart above.

This is not a new phenomenon. If you’ve ever heard the famous Warren Buffett quote “buy when there is blood in the street” then you should have a decent understanding of how sentiment controls the markets.

Sentiment can be a proxy for demand. Falling sentiment means people are less likely to want to buy as asset, leading to more sellers than buyers, sending the asset lower in price.

With the recent CPI inflation print on Tuesday this week, sentiment understandably has weakened.

All items grew at 6.4% over the last 12 months and 0.5% over the month of January. But when you look at the last twelve months most of the high inflation came in the first half.

If you take the average between July or 2022 and today, say somewhere around a 0.25% monthly change, and project that going forward the annual rate should be around 3% by June, and continue to be 3% going forward.

Three percent inflation is not bad. The Federal Reserve’s mandated target is 2% average inflation over 5 years. That means if 2022’s annual inflation was 6.5%, 2023’s is 3%, and 2024 is 2% you’ve already averaged that down to a reasonable number.

That’s to say that we don’t hit a recession, and especially a recession that actually causes more substantial month over month deflation.

Broadly the weight of inflation sentiment should be falling in market. Instead investors should be more focused on the state of the labor market, corporate earnings, and other coincident indicators.

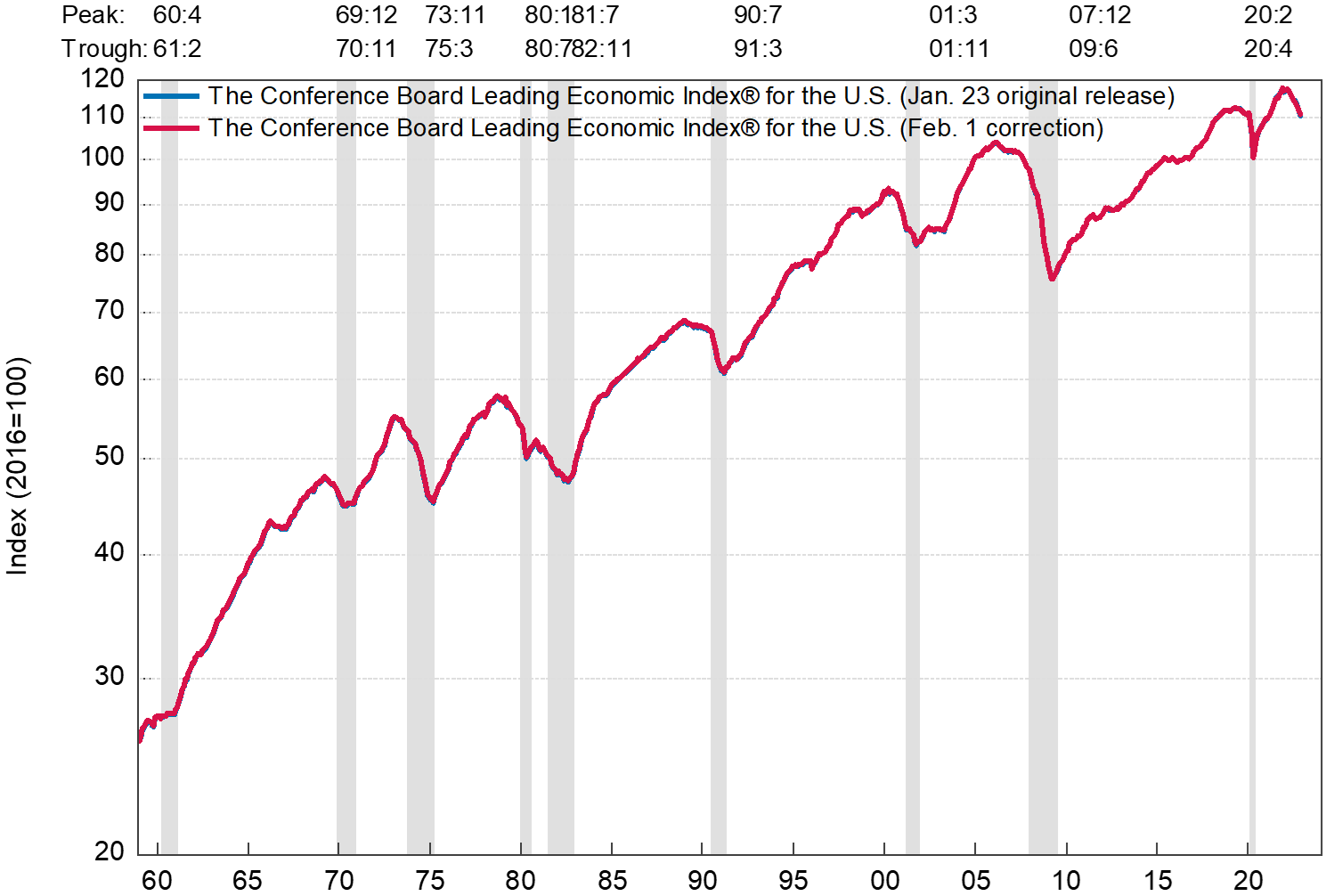

The trajectory of the US leading economic index (LEI) continues to signal a recession within the next 12 months.

The next two charts compare the business cycle using leading and coincident indicators. The while the leading variables show a notable fallback, the data has yet to be reflected in the coinciding variables.

While we are on sentiment. The leading variables matter less, because everyone has made up their minds on that. The coincident variable still have skeptics and unproven recession risks.

That’s why moving forward watching coincident indicators will be valuable for investors.