.svg)

.png)

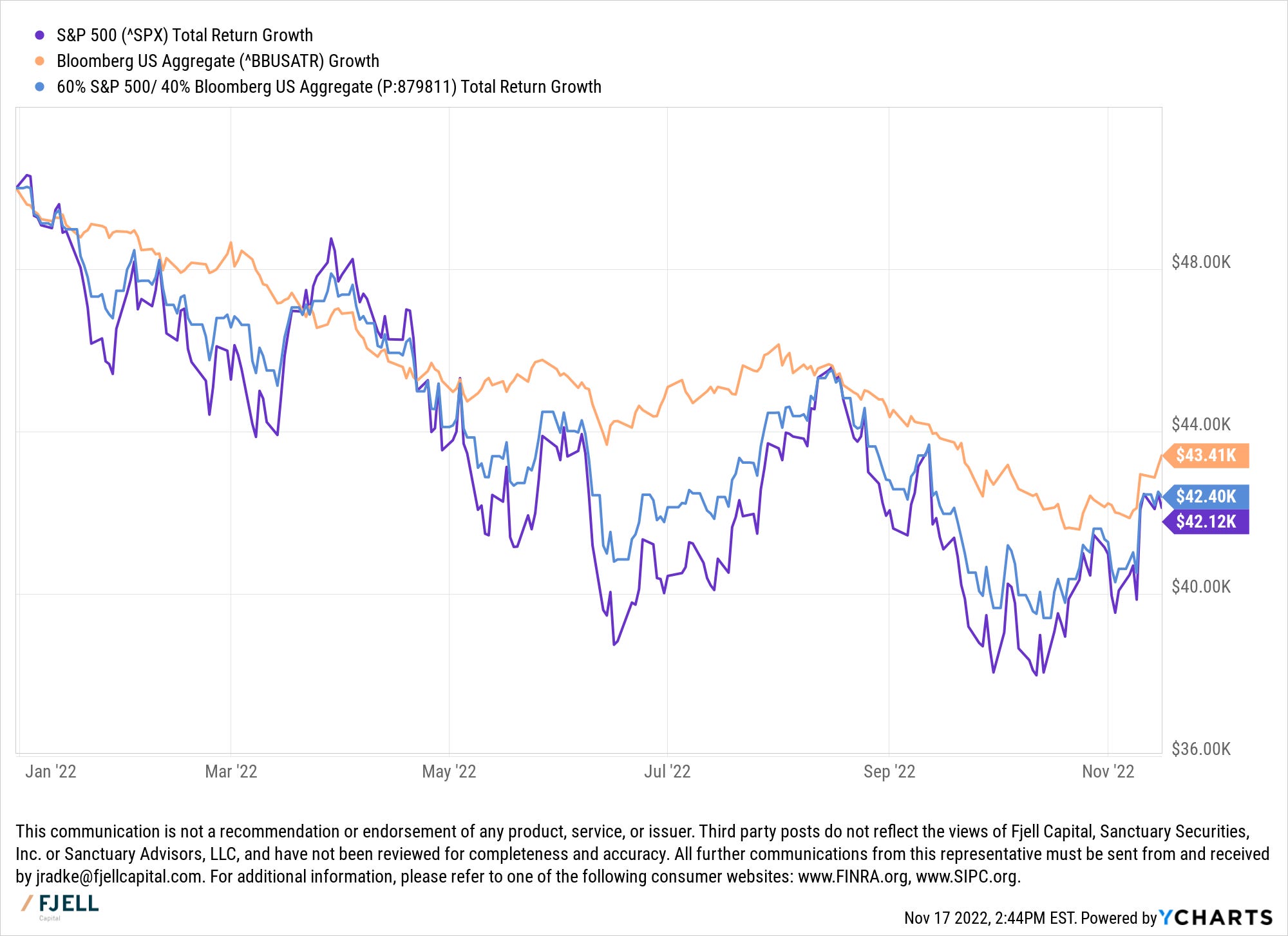

We are nearly 12 months into this bear market. But there is really no reason to think that this bear market is going to be any different than the bear markets of the past. In this post, I want to walk through the power of investing, holding through, and contributing more in a bear market.

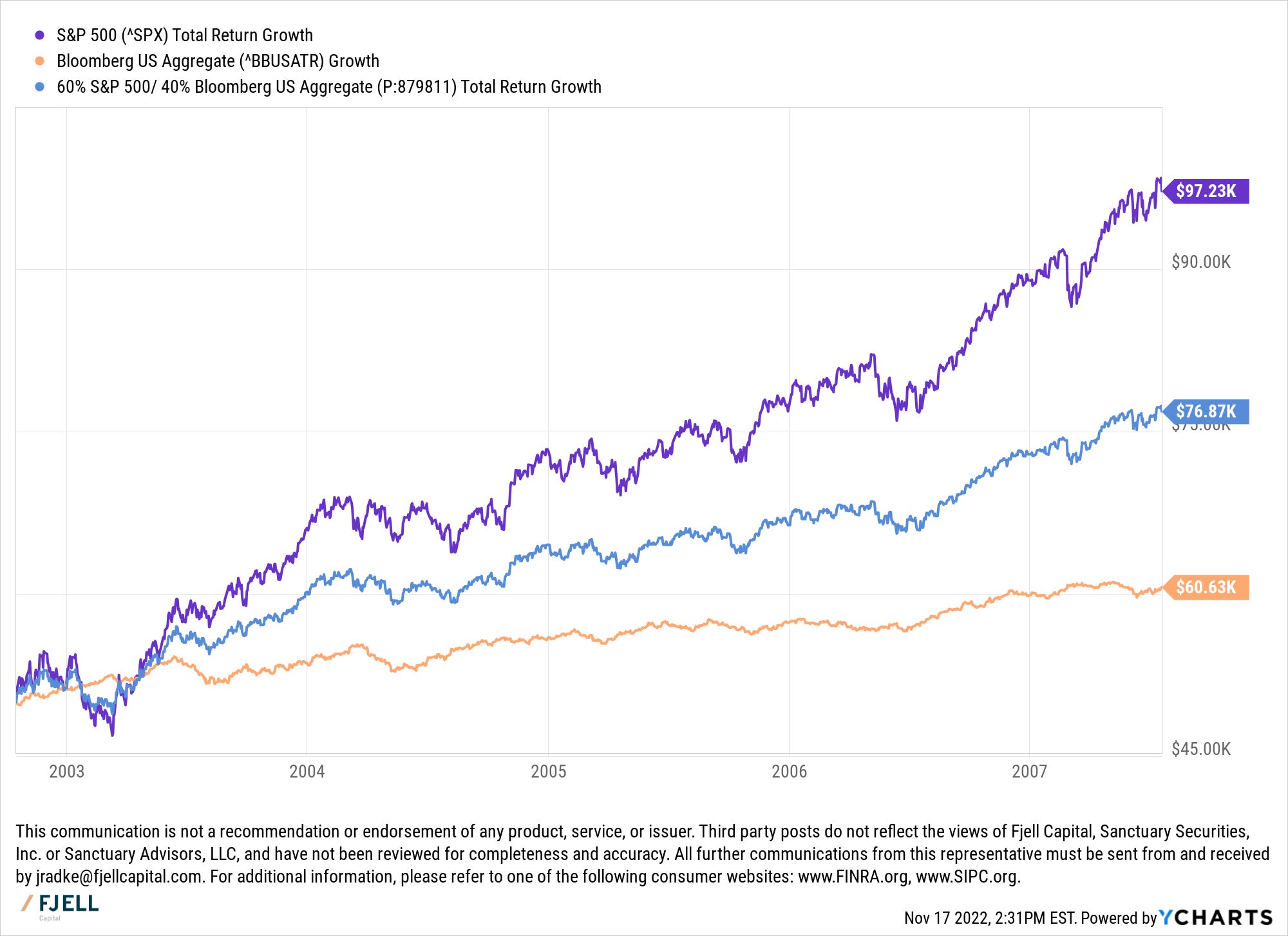

This here is the dot com bubble. Everything that had a name ending in “.com” automatically had higher valuations even though they generated no earnings. Even better were the banks that were helping them go public. Goldman Sachs alone made $4.359 billion in revenues in its investment banking segment in 1999. To put that into perspective, Goldman Sachs made $14.425 billion in 2021 in its investment banking business. $4.359 billion today would be worth $30.1 billion. Meaning in the heat of 2021s booming IPO and SPAC market Goldman made 50% less than it did in 1999.

That market would’ve sent your $50k back $20K to $30k had you invested in the S&P 500. Your 60/40 would’ve suffered a $10k loss.

Of course, once you wash out the sludge of the markets you are left with strong stable companies, whose balance sheets are both strong enough to weather the storm and capable enough to make strategic investments.

Returns following bear markets tend to still be volatile, but more volatile to the upside. What you see are large price swings back to normalization before they continue their long-term trend.

During this period you would’ve nearly doubled your $50k had you invested in the S&P 500, and saw a 50% growth on your 60/40 portfolio.

Had you invested at the worst possible day at the height of the dot com bubble, you still would’ve realized an ~$8k return on the S&P 500 and an ~$11k return on a 60/40.

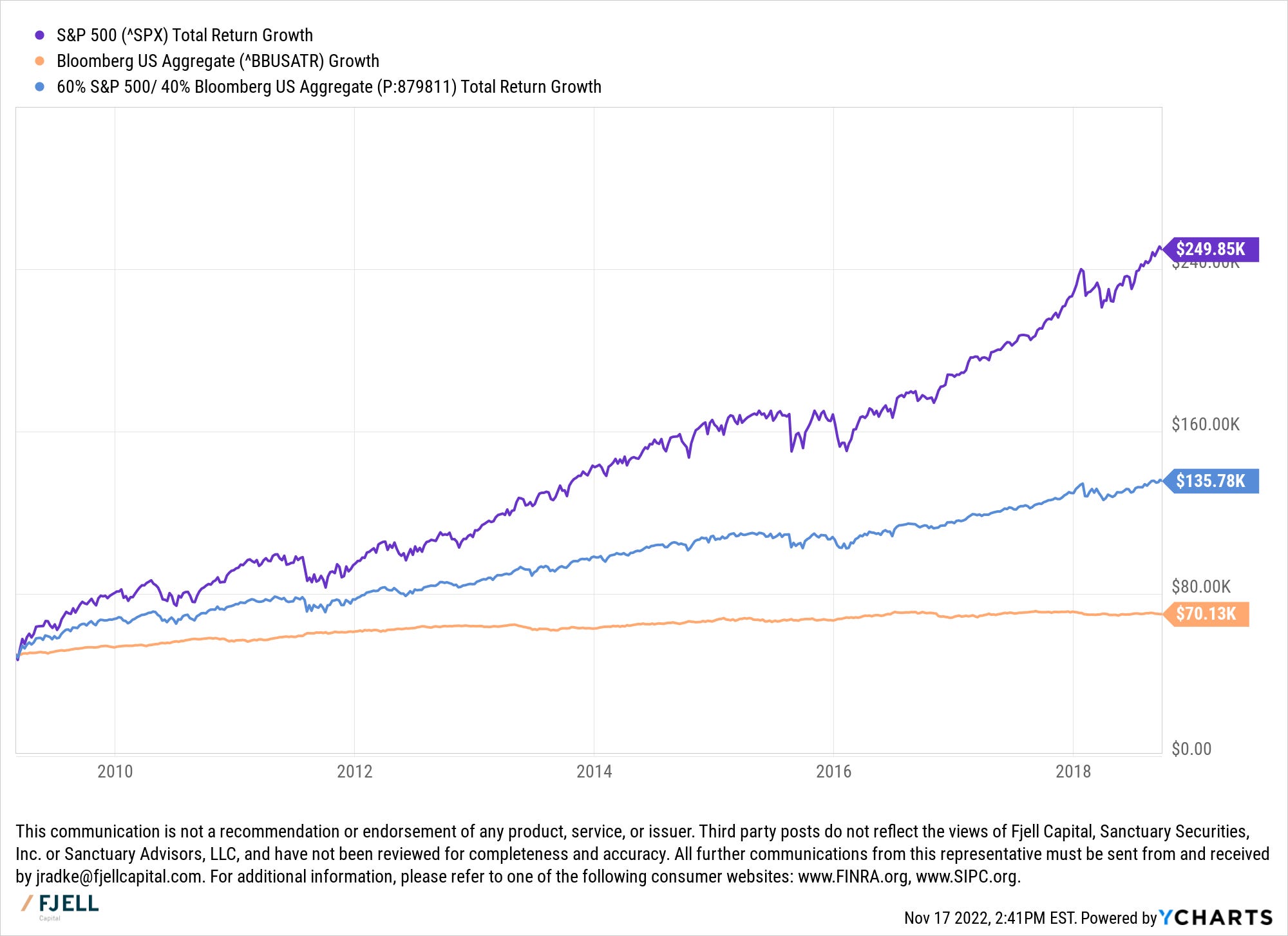

Just as those big investment banks took advantage of the dot com bubble they took advantage of the hot real estate bubble of the latter half of the first decade. Companies like Lehman Brothers took mortgages and bundled them up to make mortgage-backed securities, which is literally just a fancy word for a bunch of loans in one package since most mortgages aren’t large enough to justify the cost of selling one-off loans. As the demand for mortgage-backed securities increased the number of investment-grade mortgages to make them “investment-grade” products decreased. Eventually, mortgages were being rated and some mortgages were given as NINJA loans - no income, no job, and no assets - meaning they were essentially the bottom of the barrel.

Banks like Lehman Brothers held those MBSs on their balance sheet until they sold. When the bottom fell out and defaults rose market values for MBSs tanked and so with it the assets on bank balance sheets.

They had to be bailed out by other banks and the Federal Reserve.

Your $50k would’ve halved had it been invested in the S&P 500 and nearly a third would’ve been wiped out in your 60/40.

The Federal Reserve stepped in to provide liquidity to markets and spenders as they slashed interest rates to 0% and started buying financial assets. This couldn’t have been a better thing for companies. Had you invested in the US aggregate bond index you would’ve seen a measly $20k return on your $50k over a near 10-year period, while the S&P 500 5xed.

In the first year alone following the bear market the S&P 500 gave investors a 61% return. Of course not enough to recoup the losses experienced during the bear, but not too bad for people that contributed near the bottom.

Think not about the money you have lost but the money you could gain by contributing more in bad times.

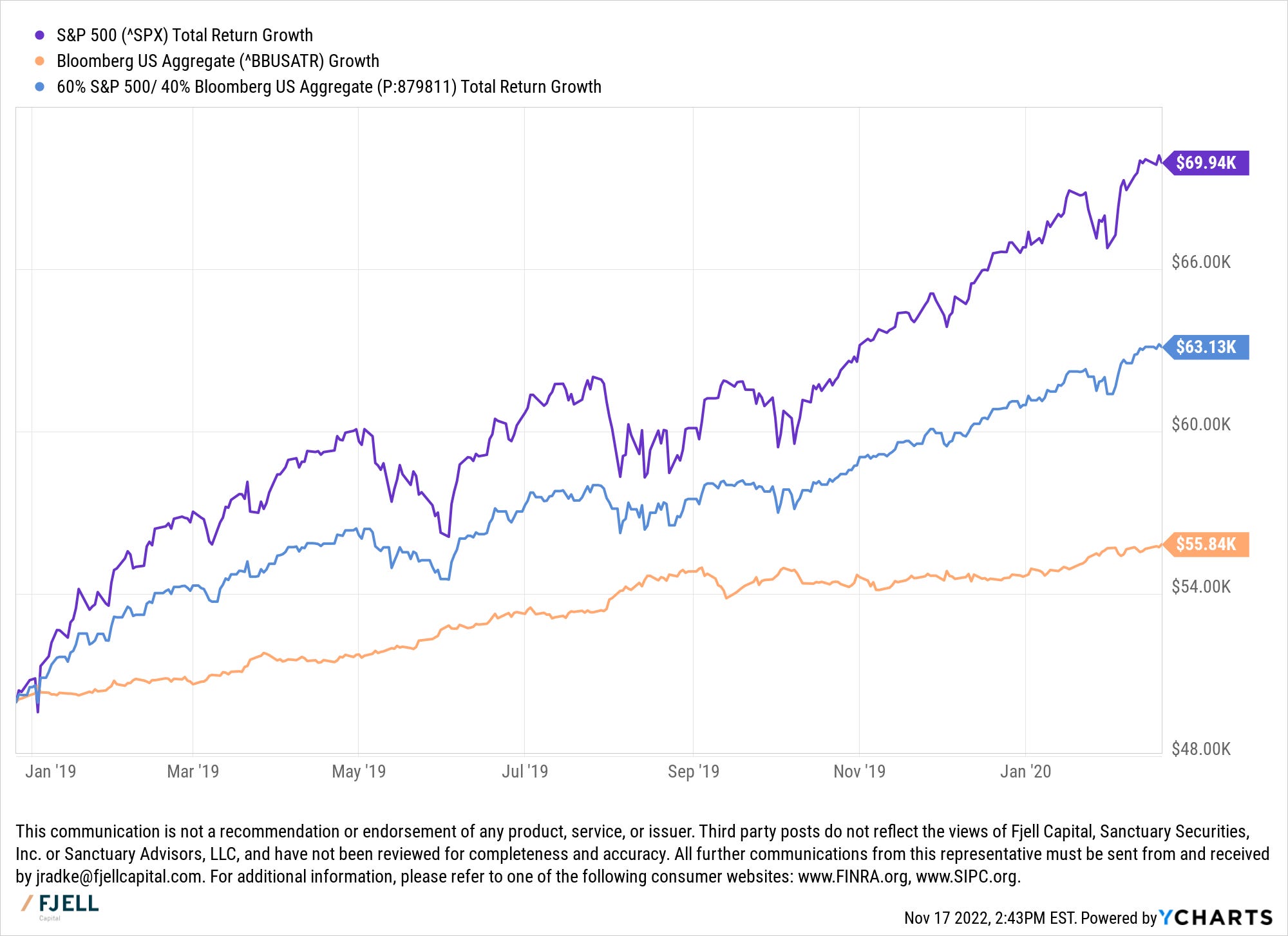

In late 2015 the Federal Reserve started raising interest rates and later start reducing the size of its balance sheet, where it held the assets it was buying, not so dissimilar to the world we live in today. Today we obviously have high inflation which is a characterization that we haven’t seen for a long time, but the Fed was raising interest rates in 2015 for the same reasons as it is today, just back then it was anticipatory versus reactive.

A lot of differences between the two markets but some similarities.

In the bull market that followed the 2018 bear (2019-early 2020) the S&P 500 returned nearly $20k on $50k and the 60/40 returned over $13k on $50k. Part of this was the pivot by the Fed. In mid-late 2019 the Fed pivots and started cutting interest rates, in anticipation the market started moving higher.

When we know the Fed will pivot markets start working towards a brighter future because the Fed pivots on recession, when that is in the mix inflation and employment fall fast. The market knows that things coming out of a recession are better than things going into one. Less uncertainty.

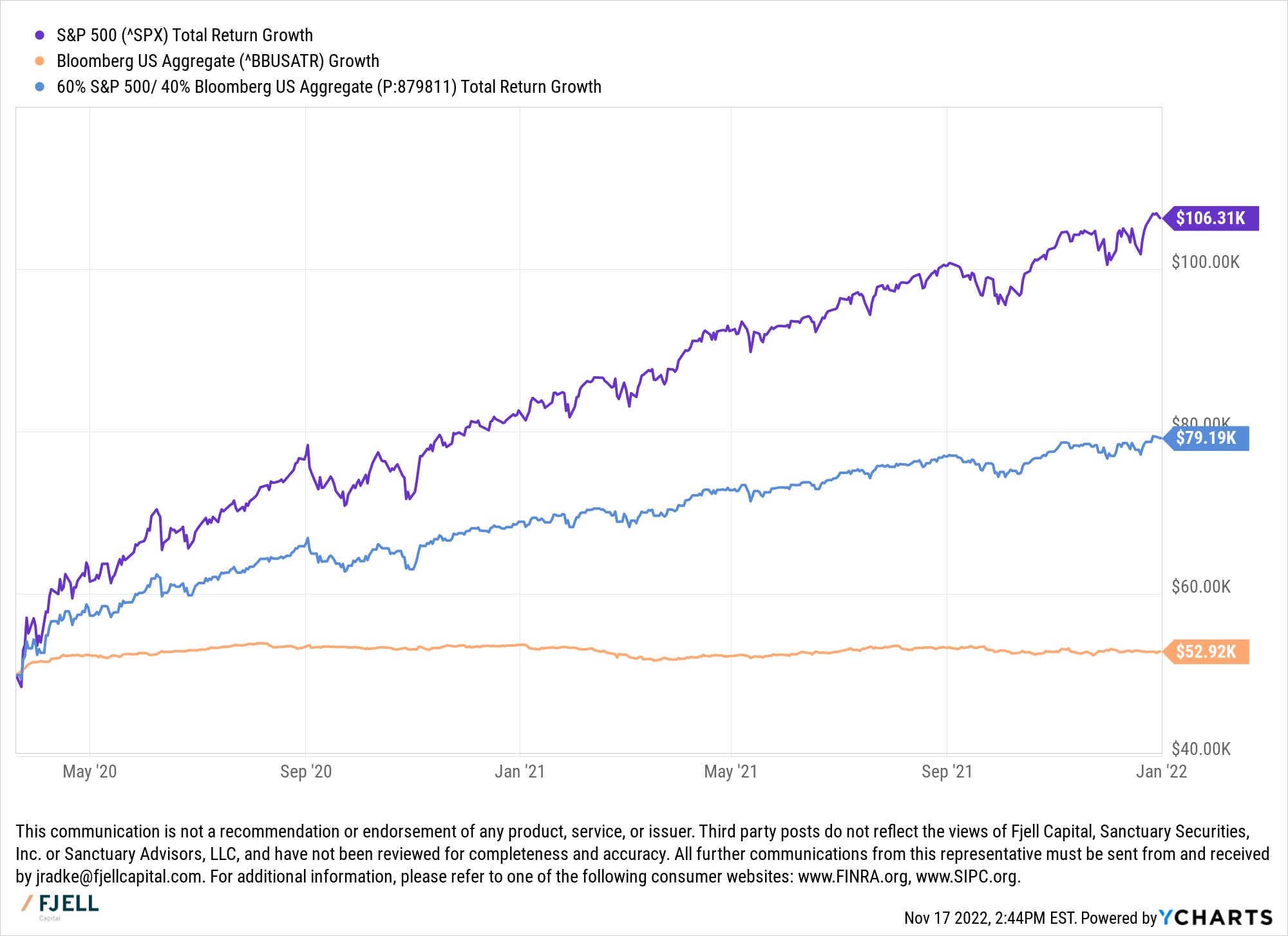

A year categorized by overspending and too much liquidity. When crypto, NFT, and Robinhood traders used free money to make risky investments that pushed the market higher, there also wasn’t any news that wasn’t better than expected, everything seemed perfect. That of course changed for some companies when interest rates started to rise. Early in the year was bad for companies that had no earnings as the 10-year treasury rate climbed back above 1%. When you’re only alternative is a bond that yields you less than a percent every year, riskier bets don’t sound so bad.

That’s also what caused the inflation. I have extra money, I spend extra money, businesses know there is extra money, they charge more.

But the tone wasn’t that the Fed would have to step in, they said it was transitory. Something investors bought into, and for a reasonable reason. Supply chains were tangled and that of course causes prices to rise.

Had you invested in the S&P 500 you would have doubled your money in less than 2 years and 60/40 would’ve earned you over a 50% return. Everyone was getting loaded because it wasn’t only stocks that went up. Houses, cars, and other things were going up as well.

Inflation no longer could keep up at the pace it was going. The Fed said late in 2021 that it would have to start increasing interest rates to bring down inflation, and thus began the largest rate hikes we’ve seen in a long time and the subsequent decline of both stocks and bonds. It’s all bad.

But a bear market is a bear market. Statistics haven’t changed because of this bear.

The has always historically come back and in full force too. As Sir Isaac Newton said, “for every action in nature there is an equal and opposite reaction”. Meaning really bad days could spell really good days in the future, as they historically have.

Forget about the money you lost and focus on the money you can gain, because if there is anything the past teaches us is that dollar costing into the market isn’t a bad thing, especially when things are bad.

Of course, this is no guarantee of future results.1

This communication is not a recommendation or endorsement of any product, service, or issuer. Posts do not reflect the views of Fjell Capital, Sanctuary Securities, Inc. or Sanctuary Advisors, LLC, and have not been reviewed for completeness and accuracy. All further communications from this representative must be sent from and received by jacobradke@substack.com. For additional information, please refer to one of the following consumer websites: www.FINRA.org, www.SIPC.org.