.svg)

.png)

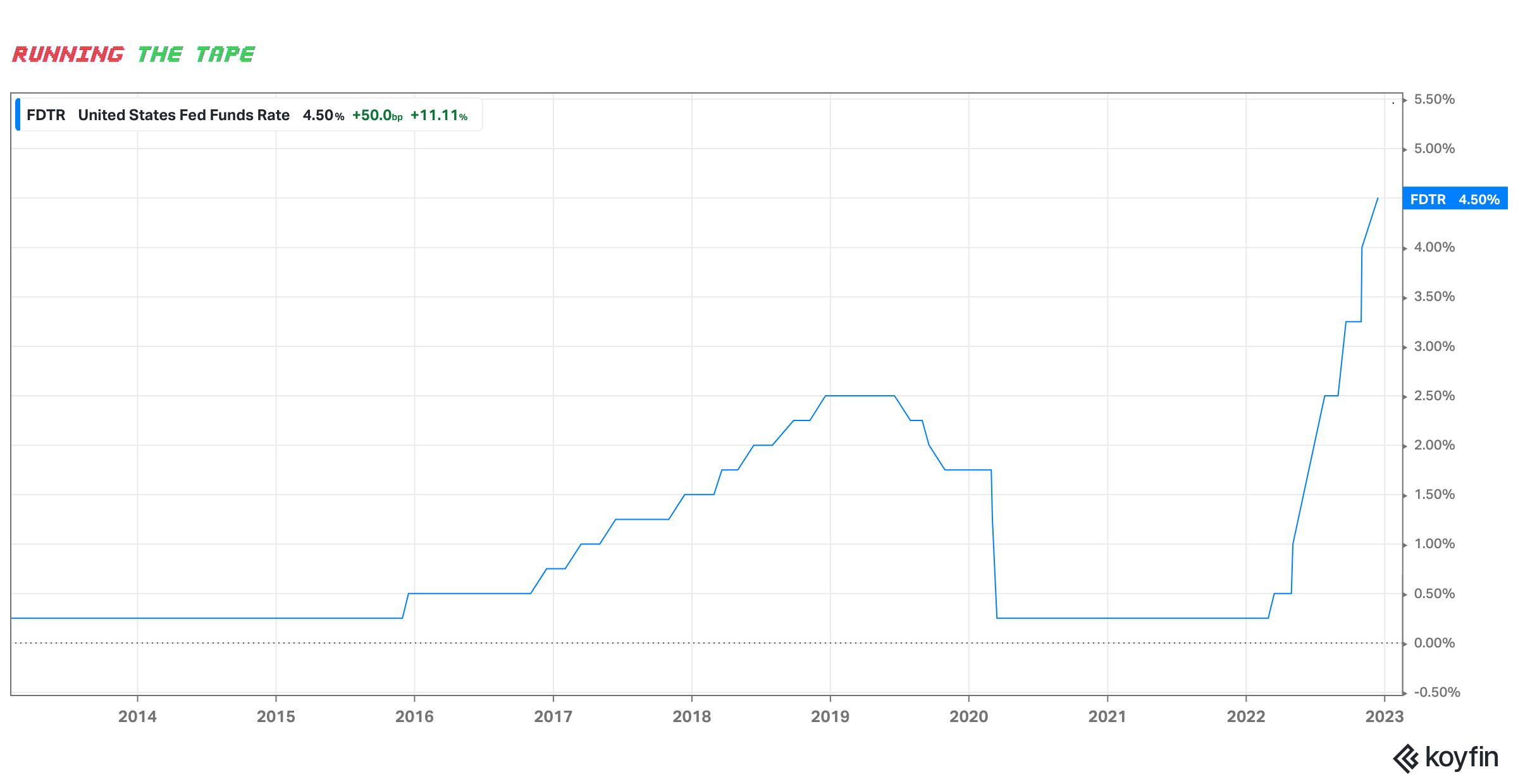

Ever since January 3rd of 2022 people have been talking about the Fed and how fast they will raise interest rates to bring down inflation.

After a historic rise in interest rates, from 0.25% to 4.5% in less than a year we now wait to see what the ramifications are in the real economy and what the ramifications are on inflation itself.

With other historic rises in the nominal Federal Funds Rate, the first thing that stands out is we haven’t seen anything like what we’ve experienced in nearly 50 years.

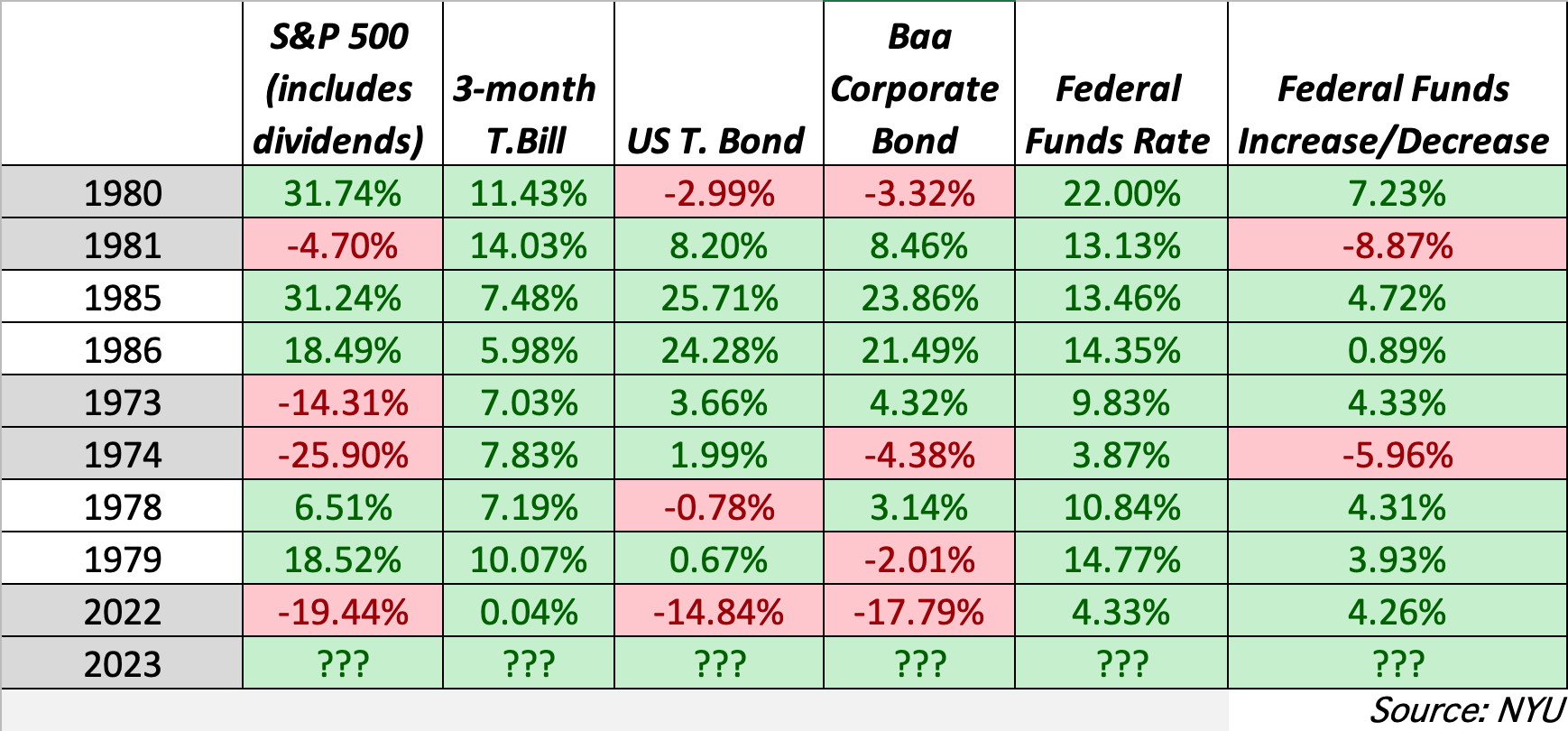

In every instance of rate increases above 4% the following years saw a recession and although this chart does not depict a recession in 1987 and 1980 it’s because rates were still rising, once rates peaked is when you saw the recession and subsequent rate cuts as we see in 1981 and 1974.

In those preceding recessions we saw a drawdown in the stock market, but what is interesting is we had a steep drawdown in 2022 whereas in other years the stock market rallied through the tightening cycle and fell in the easing cycle.

So does that mean we’ve priced in close to enough of the hiking cycle/recession that the trend will flip and we will see a rally in the easing cycle? Maybe.

Then we have inflation.

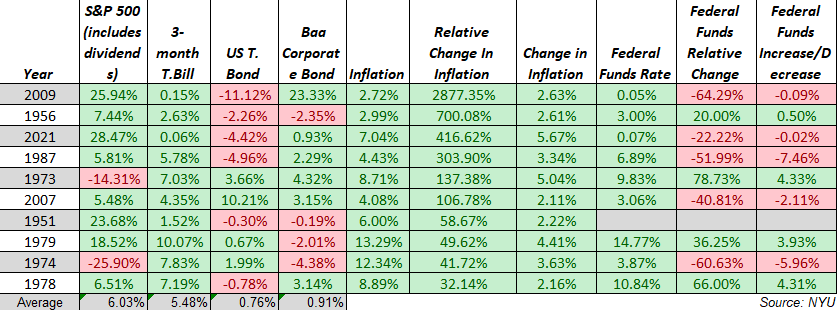

While some of the data is skewed because we see only calendar year inflation rates, meaning the rate over the course of the calendar year, it still gives a clear picture between the winners and losers of rising and falling inflation.

During times of rising inflation, the average stock market return was only 6.3%, and if you sub in 2022 instead of 2021 that average is 0.04% which is pretty much what you would expect.

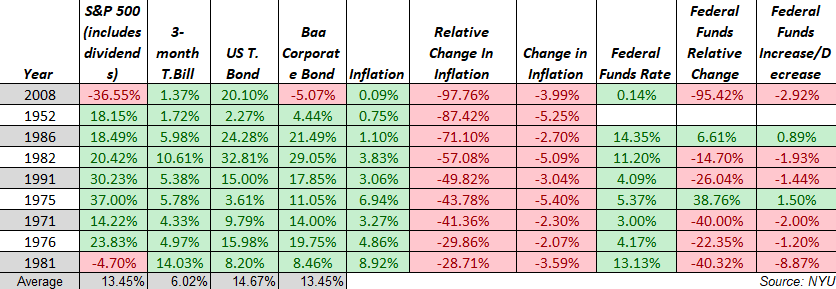

But in the case of falling inflation, the average return on the stock market was 13.45% and taking out the 2008 financial crisis which was not a year plagued with high inflation that average return is 19.71%.

We are likely currently living in a recession. Inflation generally peaks at or near the end of a recession. So with inflation peaking in June of 2022 that could be about the end of the recession, give or take 6 months.

The difference with today is the stock market has priced in most of a recession, so it doesn’t quite matter that we are living in a recession today, it only matters if it gets worse.

Inflation falls to 2% and the recession doesn’t get worse, the Fed is allowed to hold or reduce rates.

In this scenario, the stock market statistically should return 18-25% in 2023. That is what the data shows.

Inflation would fall 71%, the Fed Funds Rate would increase minimally or fall slightly.

Inflation falls to 4.5% and the recession doesn’t get worse, the Fed continues hikes to 5.25% and holds until the end of the year.

In this scenario, the stock market could return between 10-20% mostly on the fact that the recession doesn’t get worse.

Inflation doesn’t fall much from here and the recession gets worse, then the Fed has to push us into a deeper recession because inflation is still high.

This is a very unlikely scenario, but in this scenario, the stock market could see another 20-30% drawdown.

I believe the most likely scenario is scenario two. Inflation doesn’t really seem like it is going to be back at 2% anytime soon, 4.5% is a general consensus. The recession doesn’t show signs, as of right now, of getting worse. The Fed is fairly unlikely to lower rates in 2023, though that is what the better end of the range predicts.